The European Union aims to be carbon-neutral by 2050. Germany is even more ambitious: net zero by 2045 and net negative from 2050 onward. The problem is: even a massive renewables buildout and a resolute coal phaseout won’t be enough to reach these targets. This is because many industries—like steel, cement, air and marine transport—are either difficult or impossible to electrify and thus will continue to emit carbon. The only viable solution is to capture carbon emissions, permanently store them deep underground, or recycle them to make climate-neutral alternative chemicals and fuels. The latter would transform an unpopular greenhouse gas—carbon dioxide—into a valuable green resource.

CCUS is a three-step process. The first is to extract most of the CO2 from the exhaust streams of industrial facilities and fossil- or waste-fueled power plants. The second step is to apply pressure and cooling to transform the CO2 into a supercritical or liquid state, so it can be transported in trucks, trains, ships, and pipelines.

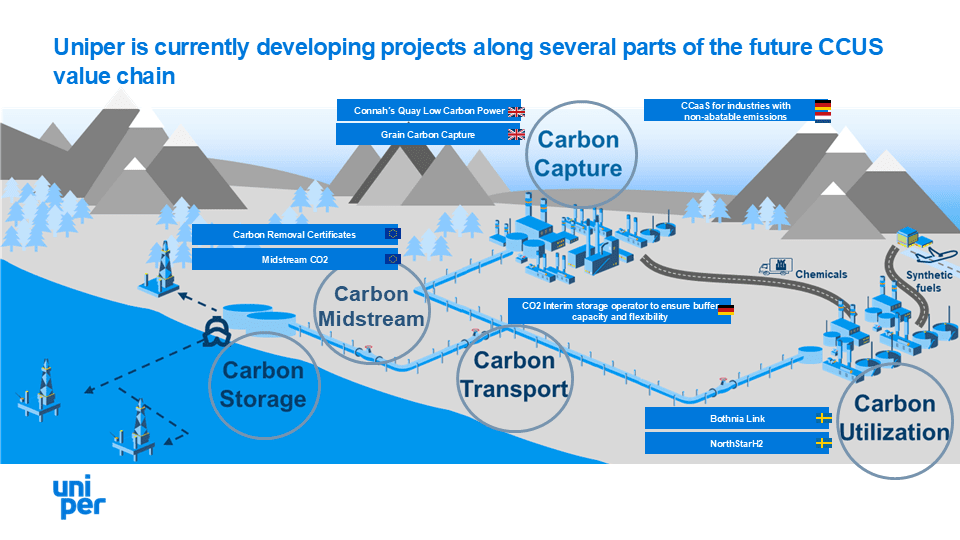

Storage, green fuels, bubbles

The third step is either permanent storage—carbon capture and storage (CCS)—or use —carbon capture and utilization (CCU). CCS is expected to be much more prevalent than CCU. The reason is that the emissions of the aforementioned hard-to-abate industries far exceed the projected demand for captured carbon. Yet CCU will play a role too. Captured CO2 can be combined with green (that is, zero carbon) hydrogen to produce a variety of synthetic chemicals and fuels for different applications—including eMethanol and sustainable aviation fuel (SAF)—or injected into soft and alcoholic beverages to make them fizzy.

CCU’s climate impact varies by source. Let’s start with products made from carbon, captured in an industrial process or power generation. Although the consumption of such projects—like when a jet plane burns SAF—releases the captured carbon into the atmosphere, this is nevertheless good for the climate. That’s because it avoids new emissions: one unit of fossil fuel first helps manufacture cement and later powers a jet plane.

Biogenic CO2—that is, carbon captured during biomass burning and gasification —is different. A jet plane that burns SAF made from biogenic CO2 and green hydrogen only releases the carbon that the biomass withdrew from the atmosphere during photosynthesis. And this carbon will be reabsorbed by the growth of more regenerative biomass. This cycle is therefore carbon neutral because it does not add additional CO2 into our biosphere. If biogenic CO2 will be permanently stored underground (BECCS), climate protection’s Holy Grail is achieved: net negative emissions, where carbon is effectively removed from the atmosphere.

Europe: same objective, different national pathways

By 2030 the EU intends to have capacity to store at least 50 million metric tons of carbon annually, which is roughly equal to Sweden’s emissions in 2022. The EU’s total potential carbon storage capacity is estimated at 260 billion metric tons, nearly two-thirds of which is offshore. More than 65 large-scale CCUS projects with a total value of over €50 billion are currently under development in Europe.

Carbon capture’s potential varies by country. The main factors are industry mix, amount and proximity of storage capacity, regulatory environment (national carbon strategy, laws, subsidies), and public support (see graphic below). The Nordic countries currently have the most favorable circumstances across all factors. Indeed, Norway, albeit outside the EU, ticks all the boxes, from strategy and legal framework to public support. Not surprisingly, it also has Europe’s most mature large-scale CCS project: Northern Lights.

Northern Lights is a cross-border, open-source CCS network. Companies across Europe can send their CO2 to be piped into safe, permanent storage 2,600 meters under the seabed off Norway’s west coast. The onshore terminal, special transport ships, and pipeline are already in place, and the first deliveries are planned to be made in 2024. In its first phase Northern Lights can likewise accept up to 1.5 million metric tons of carbon annually. Norway’s total potential carbon storage capacity is estimated to be 9.4 billion metric tons—almost 300 times its current emissions.

A similar project called Greensand is under development in Denmark. Here, permanent storage will be in a sandstone reservoir 1,800 meters below the seabed. Greensand intends to have an initial storage capacity of 1.5 million metric tons per year, which is expected to increase to 8 million by 2030. Greensand received its first carbon shipment in March 2023. In addition, Denmark is currently the only European country working on the development of onshore storage facilities.

Britain is similar to Norway: not in the EU, but systematic in its embrace of CCUS. Although Britain hasn’t yet built any assets, it has enacted applicable laws and established financial support. Britain has the advantage of starting from a favorable position: depleted offshore gas fields give it significant subsea storage potential (78 billion metric tons), while its broad industrial base encompasses many sectors that could contribute to, or benefit from, CCUS. For example, Britain intends to help decarbonize its electricity supply by capturing and storing carbon from gas-fired power plants.

In February 2024 the German federal government adopted cornerstones of a future carbon management strategy, including the approval of exploration of permanent national offshore CO2 storages. i. Nevertheless, Germany’s future role is likely to be a exporter. It has lots of hard-to-abate industries—cement, lime, iron, iron/steel, glass/ceramics, and paper/pulp—whose carbon emissions could be captured and used or exported. It’s also Europe’s largest potential market for carbon recycling in chemicals production. By 2045 Germany could contribute nearly 70 million metric tons per year to Europe’s CCUS objectives.

The Netherlands is similarly dubious about onshore carbon storage, but more open to storing it offshore in depleted gas fields. It too has a strong chemicals industry and thus good potential for carbon use.

Uniper and CCUS: it’s a gas

Uniper is well positioned to play a key role in a future carbon market. We have years of experience testing carbon-capture technology at three of our power plants. We have decades of experience in sourcing, trading, storing, and marketing gas. And we have about 550 customers in energy-intensive industries that will likely benefit from CCUS, either to capture their emissions or to use capture-derived products to replace fossil inputs in their production processes. In other words, CO2 is a gas—and Uniper knows gas.

Carbon capture: green power, blue hydrogen, and cleaner industry

Our gas-fired power plants can swiftly alter their output and thus will remain essential for maintaining a stable power supply when renewables production fluctuates. By 2050 at the latest, they’ll have to be net zero. We’ve already achieved this for two plants by converting them to run on biofuel and are testing hydrogen-firing at others. But we’re also drawing on our extensive carbon-capture experience to test this technology at Grain, our 1.3 GW gas-fired power plant in southeast England. The solution involves capturing up to 95% of Grain’s emissions for permanent offshore storage in depleted gas fields. Our conversion and CCS projects are part of our ambition to become one of Europe’s leading providers of flexible green power.

Almost all hydrogen is currently grey—that is, made in a high-emission thermal process that breaks down methane (CH4) into hydrogen (H2). Carbon capture can remove 80% of these emissions, rendering grey hydrogen climate-friendlier; in this case it’s called blue hydrogen. Uniper is currently partnering with a large oil & gas company in a project called Humber H2ub to build a blue hydrogen facility at Killingholme, our gas-fired power plant located in the Humber Industrial Cluster in northeast England. The captured carbon—up to 1.2 million metric tons per year—will be permanently stored 3,200 meters below the seabed. Many existing grey hydrogen facilities could be made blue by being retrofitted with CCS. We therefore believe that blue hydrogen is a promising interim decarbonization option until enough green hydrogen capacity is operational.

We also see opportunities to leverage our technological expertise to provide carbon-capture services to our industrial customers, many of which will be compelled—either by law or concerns about their reputation—to decarbonize their unavoidable production processes. We could do this for them by installing, owning, and operating carbon-capture equipment at their facility and by arranging for the captured CO2 to be transported for storage or use. The potential market for this service is huge. Germany’s cement, lime, and waste-incineration sectors alone are estimated to emit 30 million metric tons of unavoidable CO2 annually. As with many CCUS business models, however, carbon-capture services can only flourish if the regulatory environment changes and the required transport infrastructure is in place.

Carbon midstream: becoming a sought-after carbon-management player

Europe already has a CO2 market. Many breweries, for example, carbonate beer with CO2 that was a by-product of fertilizer production. But as captured CO2 gradually replaces fossil-based carbon as a feedstock (in other words, a raw material especially as the whole chemical industry is based on using carbon) for industrial processes, Europe’s CO2 market could grow exponentially.

Uniper can leverage its capabilities in commodity trading to support carbon management in this market by bringing together CO2 producers and users (which are often referred to as “sinks” because, like the oceans and vegetation, they absorb CO2). Our wide base of industrial customers—which in the years ahead will increasingly need to capture their carbon emissions or source captured carbon—gives us excellent access to both. We’re ideally positioned to organize offtake from CO2 sources and delivery to sinks. We could also act as a wholesale trader, including of future biogenic CO2 that complies with the Renewable Energy Directive II, the demand for which will be particularly high.

Carbon storage: serving as a carbon buffer

The thriving CO2 market necessary to decarbonize many European industries will require considerable interim capacity for storing CO2 arriving from sources and waiting to be delivered to sinks. Uniper—Europe’s fourth-largest gas storage company—operates nine underground gas storage facilities in Germany, Austria, and Britain with a total capacity of about 7.4 billion cubic meters. This gives us deep experience using storage to balance supply and demand and arbitrage prices. As the CO2 market grows, storage capacity will need to grow at similar pace so that CO2 storage—like underground gas storage—can help insure supply security.

Large-scale underground interim CO2 storage will be essential for Europe’s climate ambitions and for our own plans to serve as a midstream carbon player. That’s why we’ve already partnered with the DBI Group research institute to conduct a feasibility study. The findings show that interim CO2 storage in converted underground salt caverns is technically feasible and that its costs are comparable with cavern storage of natural gas. Our study was based on a hypothetical facility consisting of several caverns that could store between 200,000 and 400,000 metric tons of CO2 each and are connected to a single above-ground injection and withdrawal unit.

Carbon use: sustainable chemicals and fuels

Uniper has more than a decade of experience testing renewable-powered electrolysis units that split water into hydrogen and oxygen. Green hydrogen can be combined with captured carbon—ideally biogenic carbon—to manufacture climate-friendly chemicals and fuels. This promising—indeed, exciting—solution has the potential to help render hard-to-abate industries like air transport more sustainable. Below are four Uniper projects that are making this solution a reality. Depending on the project, we’re making the hydrogen, capturing the carbon, or both:

- We also plan to provide renewable-powered electrolysis units for two other eMethanal projects in Sweden: NorthStar H2 (in Östersund in central Sweden) and Bothnia LinkH2 (in Luleå, a port on the Gulf of Bothnia in northeast Sweden). Green hydrogen from the latter could also be used as a marine fuel. Together, the two projects could reduce Sweden’s annual carbon emissions by up to 310,000 metric tons.

- SkyfuelH2: Located in Långsele in east-central Sweden, this project will combine green hydrogen produced by Uniper with carbon from regenerative biomass to make sustainable aviation fuel (SAF) on an industrial scale. SkyfuelH2, the first project of its kind worldwide, could meet 10% of Sweden’s aviation fuel needs and reduce GHG emissions by 323,000 metric tons per year.

Together, these projects would reduce GHG emissions by a total of more than 0.6 million metric tons annually. As the Project Air comparison shows, that’s like taking 700,000 cars off the road every year. Uniper has a growing pipeline of carbon-use projects that leverage our hydrogen and carbon-capture expertise.

Conclusion

The European Union intends to capture at least 50 million metric tons of CO2 annually by 2030 and 450 million metric tons by 2050. The latter figure is roughly the current emissions of France and the Czech Republic combined. We believe that Uniper can provide key solutions that help expand Europe’s carbon market and thus make it possible to achieve these objectives. We can draw on our extensive experience capturing CO2 from exhaust streams to provide carbon-capture services for customers a wide variety of sectors. Our commodity-trading and gas-storage capabilities position us well to serve as an intermediary between CO2 producers and users. Finally, our expertise in green hydrogen production enables us to partner with industrial companies to manufacture climate-friendly chemicals and fuels, thereby making use of non-abatable emissions.

CCUS—which is indispensable to net zero—still has a long way to go. But Uniper has precisely the capabilities to help make it a reality.